A cut in crop forecasts for the world and the United States in September’s U.S. Department of Agriculture World Agricultural Supply and Demand Estimate (WASDE) report added to a positive tone for rice prices around the world, in a market already buoyed by crop concerns in some of the major exporters.

The USDA’s Sept. 12 WASDE report described a U.S. outlook for 2019-20 with “much lower supplies, reduced domestic use and exports, and lower ending stocks.” In the report, the USDA cut its figure for 2019-20 U.S. opening stocks to 1.42 million tonnes from its previous estimate, made a month earlier, of 1.61 million. It cut production to 5.95 million tonnes from 6.52 million. Ending stocks are forecast at 1.14 million tonnes, compared with the previously predicted figure of 1.5 million. The September Crop Production Report showed lower production area and yields. The reduced area is “the result of excessive precipitation at planting time, especially in the upper Mississippi River Delta,” the USDA said.

For the world, the USDA cut its rice crop forecast for 2019-20 to 494.22 million tonnes, down from August’s prediction of 497.86 million, with the main change being a 3-million-tonne cut in forecast Indian production. World exports were cut to 45.12 million tonnes from 46.64 million, with India’s sales abroad down by 800,000 tonnes.

“Global consumption is cut 1.2 million tonnes, and world ending stocks are lowered 1.9 million tonnes to 172.7 million, but both remain record large,” the USDA explained.

“Given the bullish revisions in the September WASDE report, the jump in futures pricing didn’t surprise anyone,” the U.S. Rice Producers said in its Rice Advocate publication.

The USDA’s Grain: World Markets and Trade Report, published Sept. 12, said that over the past month, export quotes for Thailand and Vietnam diverged further.

“Thai quotes climbed to $422/tonne on tighter exportable supplies, while Vietnam prices plunged to $321/tonne,” the USDA said. “Meanwhile, Indian and Pakistani quotes nearly converged in the middle of Thai and Viet values at $370/tonne and $360/tonne, respectively. In contrast, U.S. values rose to $555/tonne on reduced prospects for new-crop supplies, and Uruguay quotes remained constant at $528/tonne.”

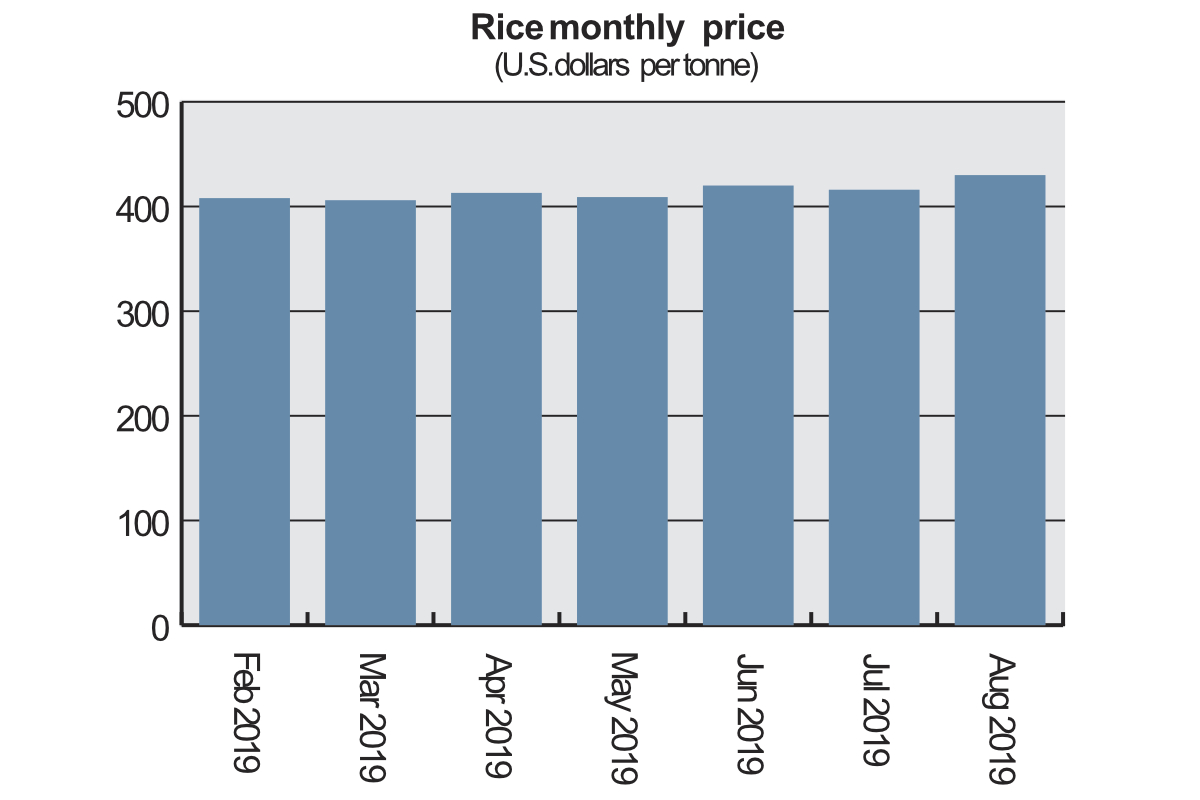

In a commentary to the FAO’s Rice Price Update for September 2019, published Sept. 5, the U.N. organization said that its price index for August was up by 1.1% from the same month the previous year.

“Across the major market segments, the most pronounced price increase took place in the fragrant market during August, lifting the Aromatic sub-index by 3.8% month-on-month to its highest since October 2014,” the FAO said. “Prices of higher and lower quality Indica rice also edged up by about 1% each, while Japonica quotations leveled off.

“Even though fresh demand remained limited during August, export quotations strengthened in most Asian origins and segments, reflecting thinning availabilities ahead of major crop harvests. In Thailand, the seasonal tightness was exacerbated by concerns over the impact of rainfall shortfalls on 2019 crops.

“Although the firmness affected most Thai qualities, it was especially evident in the Thai glutinous market, where August prices of 10% glutinous rice surged 34% over July levels to a high of $1,424 per tonne.”

The FAO also described a firmer undertone in the U.S. long grain market as harvesting started, noting “sentiment buoyed by previous sales to Iraq and other regular buyers.” In South America, prices fell to four-month lows, “pressured by sluggish demand and currency movements.”

The FAO pointed out that despite firmer prices in August, international rice prices in the first eight months of 2019 were 2.1% down on their level in the same period in 2018.

The IGC’s Grain Market Report, published Aug. 29, described international rice prices as mildly stronger on the month, “amid crop concerns in key exporters, although gains were pared by weak export demand, leaving the IGC’s rice price index broadly unchanged.”