The market for vegetable oil has moved sharply higher so far this year, with continued concerns over tight supplies as weather limits the progress of harvesting in South America and developing crops in the Northern Hemisphere.

The United Nations Food and Agriculture Organization (FAO), in its Food Price Index for March, published April 8, said vegetable oil prices were up by 8% in March compared with February, reaching their highest level since June 2011.

“The persistent strength of the index was driven by higher values of palm, soy, rape and sunflower oils,” the FAO said. “International palm oil prices registered a 10th consecutive monthly increase, as lingering concerns over tight inventory levels in major exporting countries coincided with a gradual recovery in global import demand.”

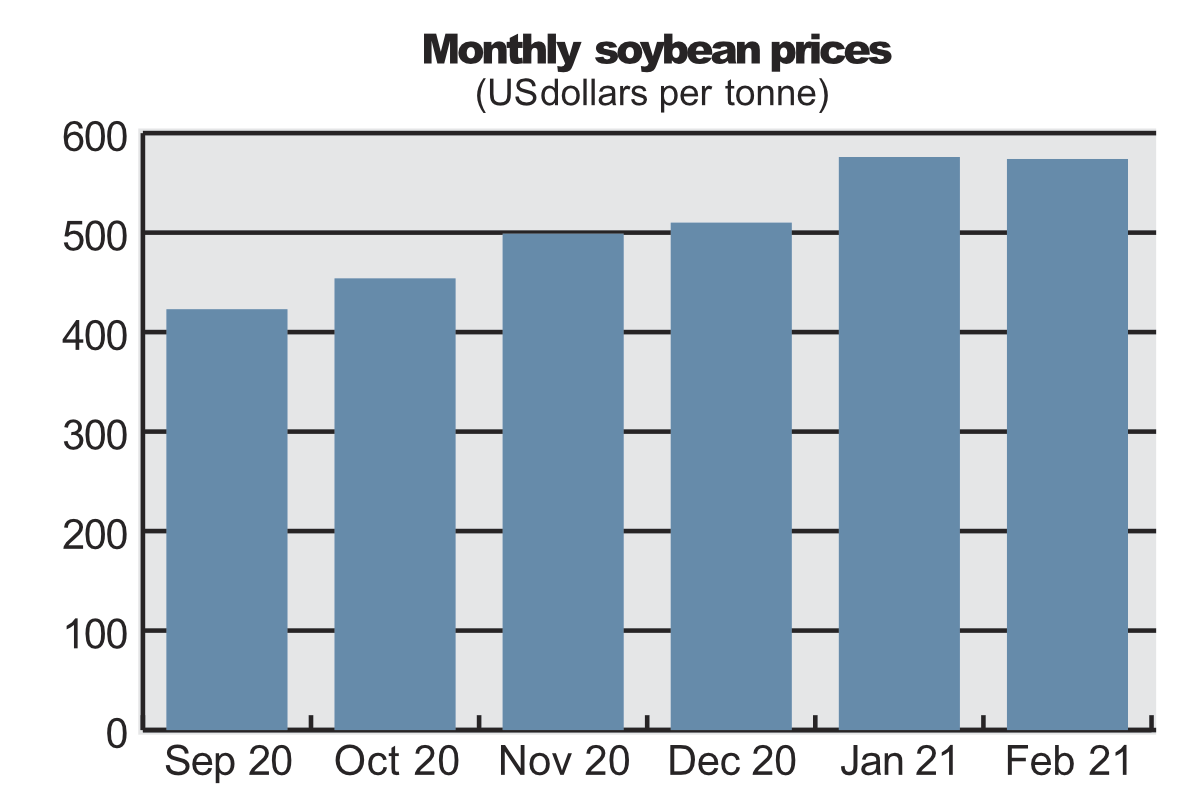

Meanwhile, soy oil prices rose sharply, largely underpinned by prospects of firm demand, especially from the biodiesel sector.

As for prices of rapeseed and sunflowerseed oils, protracted tightening supplies in, respectively, Canada and the Black Sea region continued to lend support.

The market stayed strong through April. In comments published on April 15, Will Ringrose, head of oilseeds at ADM Agriculture in the UK, noted that the April 9 USDA World Agricultural Supply and Demand Estimates report had “left the bulls disappointed, putting world (less China) ending stocks up at 86.87 million tonnes from its previous figure of 83.74 million.”

However, he noted that despite starting off the week heavily down, the market rebounded to where it originally started.

“US weather fears are becoming a bigger factor as the weather will have to be good to match market expectations,” he said. “Currently, US weather is looking drier than normal, with temperatures below average. The dryness is very supportive of fieldwork, but cold temperatures and lack of soil moisture could begin to reduce germination, which will ultimately reduce the size of the wheat, corn and soy crops. Canada is seeing similar issues.”

South American weather is looking dry, allowing harvest to pick up in Argentina and to be completed in Brazil, where it is all but done, Ringrose added.

“Soy oil continues to be volatile due to various factors,” he said. “The market was well supported when Egypt put in a tender for 30,000 tonnes for June delivery. However, Brazil has temporarily reduced its biofuel mandate from 13% to 10% to take some heat off the internal domestic oil price.”

The UK-based trader said MATIF (the French futures market) has seen large gains due to concerns over the effect of the cold snap on the EU crop, and new crop is at contract highs.

“Canada saw a similar effect on old crop as dry weather continues to threaten next year’s supply,” he added.

The USDA Economic Research Service (ERS), in its Oil Crops Outlook, published April 13, said that amidst reports of African swine fever and reduced demand for soybean meal, margins for Chinese crush have remained poor.

“However, increased global demand for vegetable oil and meal for animal feed are expected to propel global crush rates for oilseeds to another record year,” the ERS added. “Unsurprisingly, the largest growth in crush rates has been driven by soybean crush volumes. USDA forecasts the 2020-21 global soybean crush volume at nearly 322 million tonnes, a 4% rise in last year’s worldwide soybean crush volume.

“Total global crush volumes for soybeans, rapeseed, sunflower, peanut, cottonseed, copra and palm kernel are forecasted to reach near 514 million tonnes, a 1.2% increase from the 508 million tonnes of combined global crush last year.”

Chris Lyddon is World Grain’s European correspondent. He may be contacted at: [email protected]